Last

JPY

JPY

(%)

Securities Code : 2768

Last

JPY

JPY

(%)

(Real Time)

JPY

%

BN JPY

The second year of Medium-term Management Plan 2026 has concluded. Over these two years, we have invested around ¥300 billion while also reorganizing underperforming businesses. These were some of our focuses during the year ended March 31, 2026.

Compared to our targets, however, profit for the year (attributable to owners of the Company) amounted to only ¥103.6 billion in the year ended March 31, 2026, more than ¥10 billion less than the target of ¥115 billion. In this manner, we were unable to live up to the expectations of the market. Although it is true that our businesses are performing well, it is also true that some of these businesses posted losses in the year ended March 31, 2026. Earnings contributions from new businesses were able to compensate for these losses to a certain degree, but they were not enough to completely offset the losses. We also had to record some one-time losses as part of reorganizing underperforming businesses. These factors caused performance to diverge from our targets.

We wanted to take care of those underperforming businesses before they became a burden on future operations, which is why the losses were incurred. From the perspective of doing what had to be done during the second year of the medium-term management plan, I do not feel like the losses were an overly negative development. We have been investing and divesting at the same time, and this has been changing the contents of our business portfolio.

I have met with a number of investors since the announcement of Medium-term Management Plan 2026.

These meetings have shown me that their overall understanding

of the direction of Sojitz’s initiatives has been

growing steadily. I have also received feedback from

multiple investors applauding how Sojitz is increasing

earnings power across its businesses, as opposed to focusing

solely on profit growth through acquisitions. There has

also been a great deal of praise for our asset replacement

efforts in relation to underperforming businesses.

Meanwhile, common questions that I get in many of my

interactions with investors pertain to Sojitz’s ability to

accomplish return on equity (ROE) of 15% and the

approaches that will be used to reach this target.

Medium-term Management Plan 2026 earmarks ¥600 billion for investment. Over the first two years of the plan, we conducted investments totaling around ¥300 billion, and we expect to be able to invest about ¥200 billion in the final year of the plan. We will not be using the remainder of the investment budget just because it exists. Our goal is not simply to invest in line with our initial budget; we are committed to seeking out and investing in highquality projects. Moreover, we are not looking to invest in individual, standalone businesses, but rather to focus investments on those businesses where we can envision clear paths to success with the possibility of developing revenue-generating clusters of businesses (Katamari). During the initial screening process, we seek to verify whether an investment has the potential to clear our hurdle rate as well as to produce return on investment (ROI) of 10% within five or so years. After investment, we will check up on these businesses, and those for which performance has deviated from targets by more than 30% will be placed on a priority monitoring list. If a business on this list fails to achieve return on invested capital (ROIC) or cash return on invested capital (CROIC) of more than 6% within the next three to five years, we may make the decision to divest. In this manner, we are implementing structural reforms to increase earnings contributions from investments conducted prior to the start of the current medium-term management plan, for which numbers have been down. As for investments made under the current plan, our rigorous screening process is expected to result in ROI of 6.5% in the year ending March 31, 2027. This will represent a significant improvement from the level of 2% seen in the year ended March 31, 2025. Considering that some projects are still in their initial phases, we are targeting ROI of around 10% in the future.

In business areas where we are doing well, our operations will give us access to new business opportunities, increasing the range of projects we should get involved in. At the same time, there may be those projects that we feel a desire to engage in despite their lacking sufficient profitability or potentially taking a long time before they start producing returns. While I do not want to completely deny the possibility of getting involved in such projects, we cannot hope to improve ROI if this is the only type of project we invest in. Accordingly, it is crucial that we practice financial discipline throughout all stages of investment, beginning with initial screening and continuing on to post-investment monitoring of value improvements. If we fail to do so, we might invite a situation in which our profitability does not increase regardless of sales growth. Our focus cannot be those projects that appeal to us or that we want to take part in. Rather, we must constantly ask ourselves if we can find a clear path to success and develop a business that we are sure will continue to grow. Continuing to ask this question, from prior to making an investment until the moment we divest, is an essential part of practicing financial discipline.

For Sojitz, CROIC is not just an indicator to be monitored; it is an important investment criterion. If a segment is not seeing increases in CROIC, we must determine whether the issue is a lack of growth in those businesses experiencing positive growth or the downward pressure of businesses undergoing negative growth. If it is the latter, we should look at replacing said assets or implementing improvement measures to heighten the performance of the entire segment.

In the year ended March 31, 2026, we focused on addressing businesses with lackluster performance through sale or withdrawal. What was most important in this undertaking was that we were proactive, rather than just sitting back until performance had gotten so bad that we had no other choice but to act. Even in cases when a business is generating profits up to our standards, there are times in which we decide to revise operations from the perspective of whether or not this business warrants the ongoing allocation of precious talent and resources for the next five or 10 years. However, we do not simply stop at divestiture from such businesses. Rather, we look for the best possible way to scale down our involvement in these businesses, which might include transferring the business to a partner that can be a more ideal owner. Meanwhile, the funds and people freed up from our reorganization of such businesses will be reallocated to areas promising greater profits or growth potential.

When considering how to address underperforming businesses, we must make absolutely certain that we avoid situations in which we do not realize that things are not going to plan or do not fully understand why this is the case. We cannot expect everything to follow our original plans. What is important is that we take corrective actions at the best possible timing when issues do emerge. We must rapidly implement a cycle of early detection of issues, corrective action, and course adjustment when that action proves insufficient. This approach will no doubt raise our success rates in developing businesses and help minimize the damages when we fail.

To accelerate decision-making and facilitate more accurate decisions, in 2025 we began sharing reviews of underperforming businesses at meetings of segment leadership. The goal of this sharing was not to just offer superficial overviews and examinations; we wanted to provide a place for discussions that get to the heart of issues and for sharing of examples of business failures.

We estimate that Sojitz’s cost of capital is between 9% and 10%. Meanwhile, we have defined ROE targets of 12% on a three-year average for Medium-term Management Plan 2026 and 15% for our next stage. An ROE of 12% is the bare minimum we need to secure an adequate equity spread and is in fact not a sufficient level overall. A cost of capital of 9% to 10% will require us to produce ROE of at least 15% to exercise freedom in management with the trust of investors. This is why we have set the ROE target of 15%, which represents the level needed to maintain our appeal when compared to other general trading companies and to practice management in Sojitz’s own unique fashion. Other general trading companies tend to have ROE of between 13% and 15%. Sojitz cannot allow itself to fall behind these competitors in terms of scale or in terms of profitability. Our target may not be easy to accomplish, but the fact that we have set this target at all is a representation of our confidence in Sojitz’s ability to achieve this goal.

Improving ROE will be crucial to lowering cost of capital. Equally important will be for us to build a reputation for Sojitz as a constantly evolving company. Our portfolio reforms are not the goal in and of themselves. Rather, we seek to build a track record of increasing the profitability and growth potential of our business portfolio through such reforms. I believe that making investors feel confident in our ability to continue to evolve in this manner will help us lower cost of capital. Similarly, our path toward reaching ROE of 15% will not be through applying financial leverage to get our numbers up but instead through strengthening our earnings power. Meanwhile, we will continue to adhere to our basic cash flow management policy of allocating the cash generated through operations and asset replacement to steady growth investment and shareholder returns.

My vision for Sojitz’s growth is not a straight line drawn by consistent growth of 10% each year in our current businesses. It is more a type of growth that breaks trends through growth spurts seen when we combine new businesses or obtain new functions. However, this does not mean that we will constantly be entering into new fields. Rather, our approach will be about identifying paths to success and building new businesses or broadening existing operations. In this manner, we will grow by refining our operations. This is what I mean by “trend-breaking growth.” The trends we break are not about the speed of our growth, which would result in sudden spikes in growth, but instead about developing revenue-generating clusters of businesses (Katamari) and branching out from there to create new Katamari. During the year ending March 31, 2027, I look to give further shape to this approach for advancing toward our next stage.

Since the announcement of Medium-term Management Plan 2026, we have continued to explain our progress while offering examples of the Sojitz Growth Story at financial results presentations. What is more important, however, is the degree to which we can tie the concepts we present to actual performance and build our track record in this manner. We cannot just be content with flashy advertisements of our most newsworthy projects. Instead, we should faithfully and consistently describe both the “goods” and the “bads” of our business in order to paint a clear picture of our road map for value creation. As for shareholder returns, we will maintain our current policy of issuing consistent dividend payments based on the ratio of dividends to shareholders’ equity. It is prudent for us to first focus on steady improvements to ROE so that we can present these gains as examples of success in crafting the Sojitz Growth Story and thereby enhance corporate value and earn higher appraisals from the market.

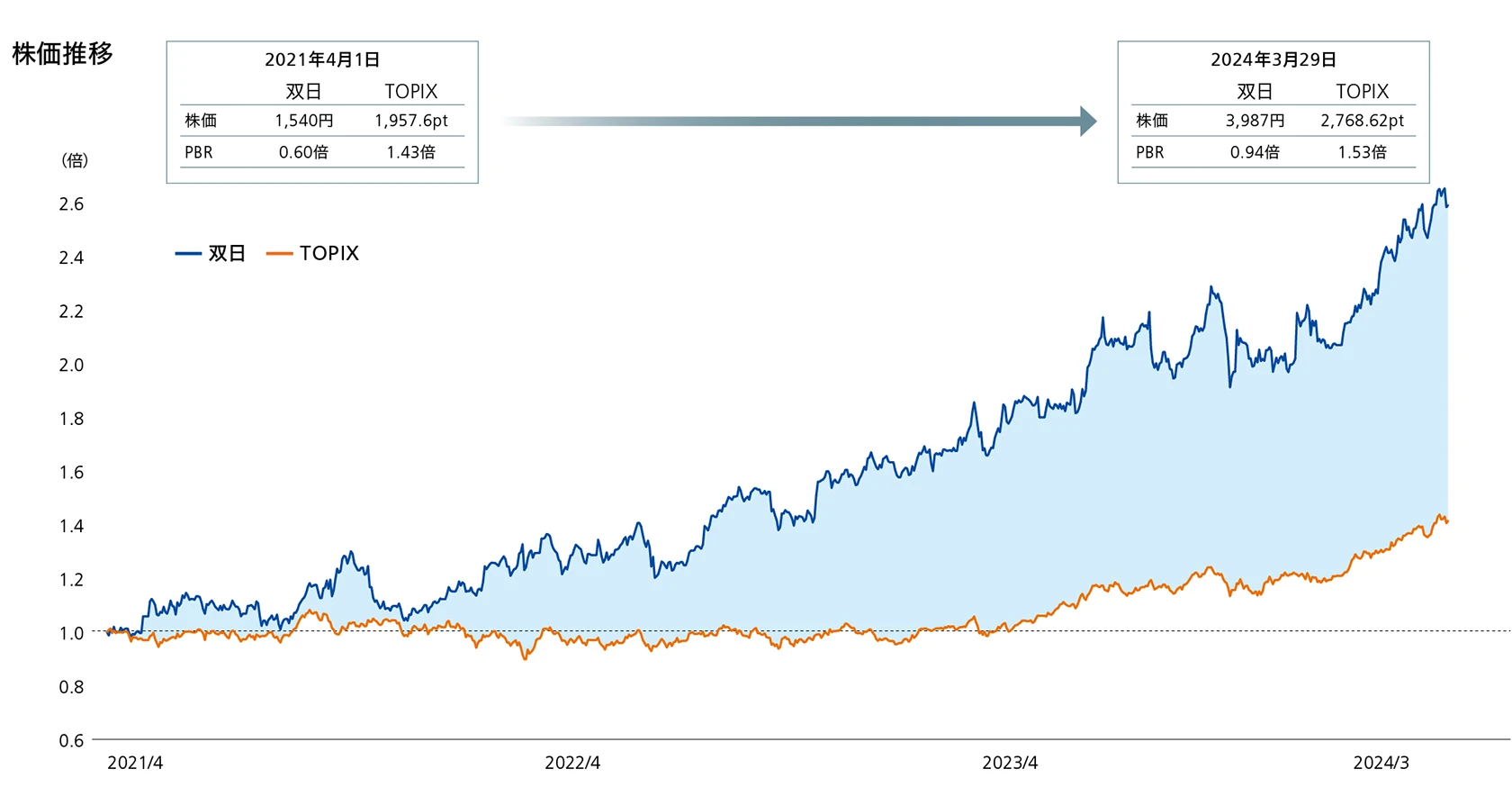

In the year ended March 31, 2026, we saw a particularly large increase in our stock price during the second half of the fiscal year. This increase is due in part to external factors, such as anticipation pertaining to rare earths and overall market recovery. Nevertheless, we must also consider the fact that, in the past, market upticks have not necessarily translated to equivalent increases in Sojitz’s stock price. For this reason, I feel that the stock price gains seen in the previous fiscal year can also be attributed to increases to the extent to which anticipation for Sojitz’s future growth and transformation has come to be reflected in our stock price.

As CFO, I have been communicating one simple message within the Company: “Make sure we generate earnings.” We have the funds and the foundations necessary to do this, so I want employees to take full advantage of our resources to produce earnings. This expectation is backed by my belief in the potential of our people. I want everyone, in both business and corporate divisions, to act swiftly and effectively to create value for themselves and for the Company. We should think and act independently and, when we fail, we should apply the lessons learned to future undertakings. If we do this, we will begin to see the connection between Sojitz’s DNA of future forecasting and preemptive action and our intellectual curiosity and inquiries for getting to the heart of matters. More capable people will be able to act with greater speed, which will result in higher earnings. This in turn will allow each and every employee to feel motivated, grow, and take their work to the next level. Ideally, I want Sojitz to become a company that is praised by all of its employees because it is able to sustain this cycle on an ongoing basis. Just as we aim to develop another two or three Katamari during the year ending March 31, 2027, cultivating the people who will create these Katamari will be an incredibly important part of wrapping up Medium-term Management Plan 2026. Everything I have talked about today—practicing financial discipline, transforming our portfolio, and improving ROE—are all things that need to be accomplished by people. President Uemura has been saying the same thing, and, from my perspective as CFO, I share his view.

We must work to accomplish what we say we will do. Steadfast effort to build our track record is the only way to earn the trust of our shareholders and other investors. I hope we can look forward to your ongoing support and understanding.

*Organization affiliations and titles are current as of July 2026.

This Website was created for the purpose of providing information relating to Sojitz corporation. It was not created to solicit investors to buy or sell Sojitz Corporation's stock. The final decision and responsibility for investments rests solely with the user of this Website and its content.

This website contains forward-looking statements about future performance, events or management plans of the Company based on the available information, certain assumptions and expectation at the point of disclosure, of which many are beyond the Company’s control. These are subject to a number of risks, uncertainties and factors, including but not limited to, economic and financial conditions, factors that may affect the level of demand and financial performance of the major industries and customers we serve, interest rate and currency fluctuations, availability and cost of funding, fluctuations in commodity and materials prices, political turmoil in certain countries and regions, litigations claims, change in laws, regulations and tax rules, and other factors. Actual results, performances and achievements may differ materially from those described explicitly or implicitly in the relevant forward-looking statements. The Company has no responsibility for any possible damages arising from the use of information on this website.

Although the information on this website is prepared with the greatest care, the Company does not guarantee the accuracy, continuity or quality of any information provided on this website or that it is up-to-date, nor does it accept responsibility for any damage or loss arising from the falsification of data by third parties, data downloads, etc., irrespective of the reasons therefore.

Please also be aware that information on this Website may be changed, modified, added or removed at any time without prior notice.